It’s a term we use frequently in new or expansion sales: product value, business value, Time-to-Value. But what is it, exactly?

It’s a term we use frequently in new or expansion sales: product value, business value, Time-to-Value. But what is it, exactly?

A broader definition

Marketers say it’s a simple equation: Value = Benefits – Cost. When the benefits outweigh the costs, something has value. Marketers regularly communicate how their product’s features, advantages and benefits are better than the competition. They posit customers always choose the product with the highest value.

But scientists say it’s more complicated. Numerous experiments show the human brain considers multiple factors when considering value:

- Context—internal and external states affect perceived rewards. For example, you may choose a hot cup of coffee on a cold day, but that same cup on a 100-degree day is suddenly less attractive. How the mind values a set of options varies by circumstances.

- Rewards—utility, or meeting practical needs, is just one type of reward. The brain also responds to how well a choice meets social and personal needs. When people are hungry any restaurant will do, but you may choose a friend’s favorite hangout to put a smile on their face.

- Probability—humans often make choices involving risk and uncertainty. Our brains automatically calculate the odds of success associated with one option or another. You may buy travel insurance when you think the odds are good a hurricane could ruin your vacation.

- Cost (or effort)—rarely do returns come without investment. The brain is wired to consider tradeoffs, weighing the cost of resources against the rewards. For instance, you may choose to buy gas near your house or drive ten minutes further to save five cents per gallon.

- Time—when benefits are to be received also factors into decision making. If you win the lottery, you face a choice between a large lump-sum and many years of smaller annuity payments.

- Preference—even after logical deliberation emotions still win the day. For example, you may consider several soft drinks on the store shelf, but you simply choose the brand you like most.

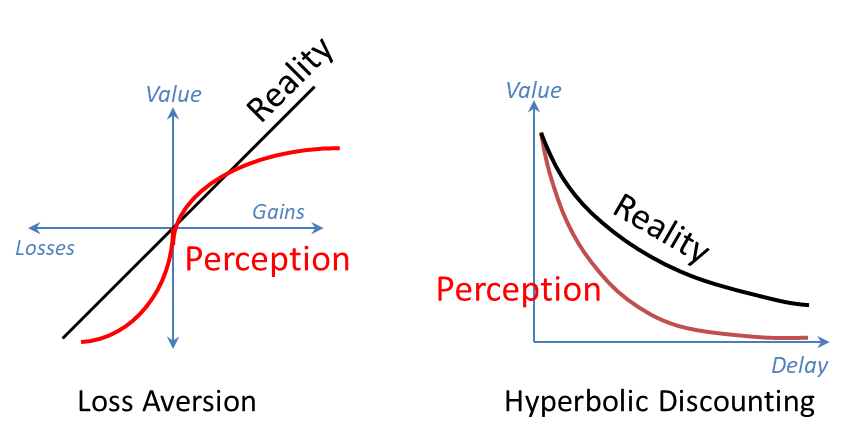

The math actually describing human choice gets messy.[1] Neuroscientists think time and risk act as nonlinear decision modulators. This means calculations like Expected Value and Net Present Value might look good on spreadsheets, but they don’t reflect how customers really decide. Prospect theory, for example, shows the human brain overestimates potential losses and underestimates potential gains, leading to irrational “loss aversion.” Likewise, humans tend to place more value on short-term than long-term wins. This causes a phenomenon called “hyperbolic discounting.” Our subconscious, emotional biases regularly distort our conscious, logical reasoning.

Neuroeconomics is relatively new, and even if we someday crack the brain’s code, reliance on prediction will always be problematic. As statistician George Box famously said, “All models are wrong. Some are useful.” Equations may predict aggregate behaviors, but at an individual level, all value is subjective. When facing the same choice, one person may value an option very differently than another.

Neuroeconomics is relatively new, and even if we someday crack the brain’s code, reliance on prediction will always be problematic. As statistician George Box famously said, “All models are wrong. Some are useful.” Equations may predict aggregate behaviors, but at an individual level, all value is subjective. When facing the same choice, one person may value an option very differently than another.

Brains in business

Neuroscience points to the types of questions each customer must answer for themselves, either explicitly or implicitly, during the business sales cycle:

- Context—Why are we making this decision? What problem are we trying to solve? How does this purchase align with our objectives? Where does it fit in our process?

- Rewards—How well does this product solve my problem? How much productivity or revenue will we gain? How will my boss view me after making this decision? What will my subordinates think? Will this make my life easier or harder?

- Probability—Will we really get the results they’re promising? Will I be as satisfied as their other customers? What could fail? What’s the worst case? Best case? How might the risks impact me?

- Cost (or effort)—How much money do I need to pay for this? How much work is involved to set it up? How many resources will I need? How hard is it to learn? How difficult is it to switch to the new way of doing things?

- Time—When must a decision be made? How long will implementation take? How soon will we see results? When can we expect a return on our investment?

- Preference—Who do I like? Who do other people like? Which vendor makes me feel the most comfortable?

Despite what Marketing says, value transcends the simple difference between product attributes and the price customers are willing to pay for them. Science shows humans also factor in context, social and personal rewards, time, risk, and personal preferences. Salespeople must understand how all of these variables impact each and every sale and recognize that choices aren’t always rational. It’s the best way to ensure the customer is making a decision that’s right for them.

Source:

[1] Talmi, D., and Pine, A. (2012) How costs influence decision values for mixed outcomes. Frontiers in Neuroscience, 26 October, 2012.